")

dizzy 3d

There is value in covering unfollowed stocks, as the market often sleeps on such stocks. This creates many opportunities for value investors willing to do their homework to take advantage of market mispricing.

like that I found this case on Urban Edge (New York Stock Exchange:UE), last mentioned here In January 2021, we noted its attractive portfolio profile, redevelopment opportunities and relative undervaluation.

The stock has fared very well for patient investors employing a buy-and-hold strategy, with the stock up 27% since our last article and a total return of 43% including dividends, trailing the S&P 500 (SPY )’s 22% rise. ) over the same period. In fact, as you can see below, UE’s total return (and stock price return) has “slightly outperformed” even the S&P 500 over the past year.

UE vs. SPY Total Return (Seeking Alpha)

This article provides an update on the stock and discusses whether it remains a buy at this point. So let’s get started!

Why UE?

Urban Edge is a retail REIT that owns both indoor and outdoor shopping destinations along the Washington, DC to Boston corridor. It currently owns 76 properties spanning 17 million square feet of gross lettable square footage.

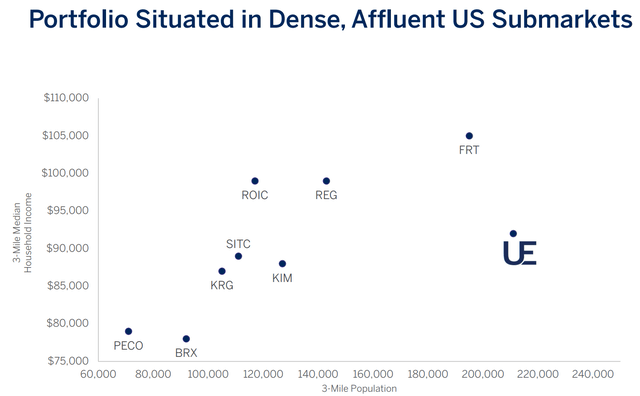

This includes 44 properties (representing 80% of the total UE) located in the densely populated New York City subway First Loop suburbs, where demand for housing and real estate is significantly higher than in other areas of the country. included. These suburban first-ring regions have primarily benefited from increased remote and hybrid work as consumers spend more time in their residences since the pandemic. As shown below, the population of UE’s 3 miles is greater than the population of Federal Real Estate Investment Trust (FRT).

Investor presentation

UE also benefits from low retail supply competition in the market. As shown below, this location leads its peers in having the highest number of households per square foot and also has one of the lowest retail square footage per household.

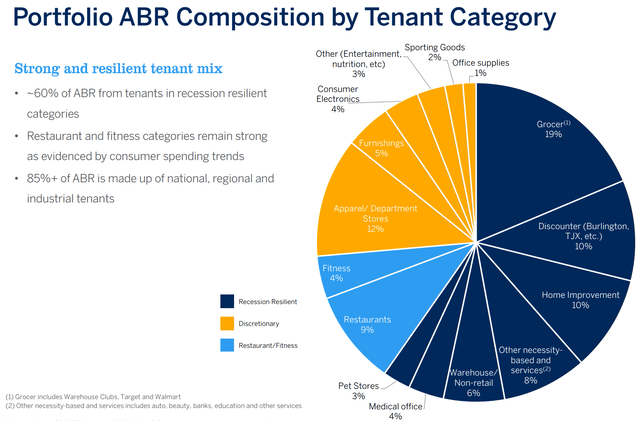

Additionally, most of UE’s annual base rent comes from tenants in recession-proof categories, which include grocery stores, discount stores, home improvement stores, and other essential goods and services, as well as warehouse stores, medical clinics, pet stores, and restaurants. accounts for 60% of that. ABR.

Investor presentation

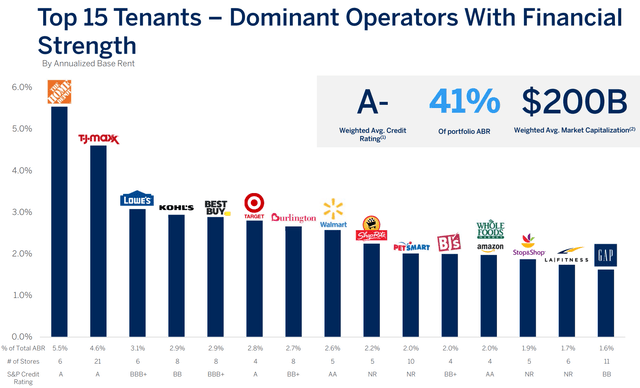

Specifically, 85% of ABR is driven by national, regional, and industrial tenants such as Home Depot (HD), TJ Maxx (TJX), Lowe’s (LOW), Walmart (WMT), Target (TGT), and Whole Foods (AMZN). Thing. It is in the top 10 tenants as shown below.

Investor presentation

On the other hand, UE’s business foundation is solid, with same-property NOI, including properties under redevelopment, increasing by 3.3% year-on-year in the third quarter and 4.5% year-on-year in the first nine months of this year. . Occupancy rates for similar properties also remained strong, increasing 130 basis points year over year to 95.0%.

UE recorded a 50bps quarter-over-quarter decline due to Bed Bath & Beyond store closures, and management is seeking interest from potential tenants to fill the gap. This shouldn’t be too much of an issue considering tenant demand for space has resulted in healthy cash rent spreads of 12.5% on new and renewal leases.

Looking ahead, the addition of Shoppers World and Boston’s Gateway Center in 2024 for $309 million at an attractive 7% cap rate could significantly drive UE’s top and bottom line growth. There is a gender. These are substantial assets that currently represent 10% of UE’s total value and represent the “dominant” retail node in Boston, as management highlighted in the last conference call.

Shoppers World is one of the most frequented open-air shopping centers in the Northeast, with more than 11 million people visiting the site in 2022. It is a large property with 92 acres and 758,000 total leasable square feet. The property is located in the heart of the Golden Triangle, a major retail hub in the Boston area. It will be anchored by Best Buy, Nordstrom Rack, TJ Maxx, Marshalls, HomeSense, Sierra Trading, Kohl’s, AMC, and a new grocery store scheduled to open in July 2025.

Gateway Center is 639,000 square feet and has a 3-mile population of more than 417,000 people with a median household income of $106,000 per year. The property is located just five miles from downtown Boston in a rapidly densifying area and sits on 89 acres with over 3,000 parking spaces. Tenants include Target, Costco and Home Depot.

UE’s management was able to dispose of its industrial property last year at a low cap rate of 4.9% (significantly below the acquisition cap rate of 7% mentioned above), thereby increasing its ability to repurpose capital to fund growth. is also shown. In 2024, UE plans to dispose of non-core real estate in the industrial, self-storage, and single-tenant categories totaling $100 million at a cap rate range in the low 5% range, so I expect such disposals to be I’m going to look for more.

Risks to UE include the potential for macroeconomic challenges this year, as consumer spending has slowed in recent months, presenting potential challenges for UE’s retail tenants in the short term. Masu.

Additionally, UE is expected to have net debt-to-EBITDA of 6.6x for the full year 2023, giving it slightly higher leverage than the 6x level that rating agencies generally consider safe. However, management expects leverage to be below 6.5x this year due to rental initiation in the redevelopment pipeline. UE’s debt maturities are also well-staged, with just 19% of its debt maturing between now and 2026, compared to a peer average of 40%.

Importantly for dividend investors, UE pays a dividend yield of 3.5%, which is more than covered by its 52% payout ratio, leaving plenty of room to pay down debt and reinvest in the business. It means that it is.

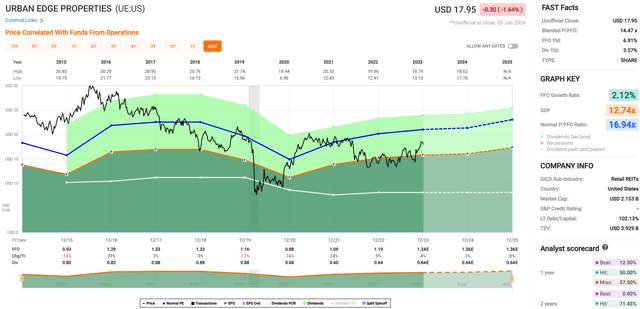

We also believe there is value in UE at its current price of $17.95 and forward P/FFO of 14.5, below its typical P/FFO of 16.9. Analysts expect FFO/equity growth to be only 2.2% this year, but given the desirable location and strong lease spreads in the portfolio, UE expects at least mid-single-digit annual FFO growth over the long term. /I see it as having the potential to generate growth for the stock. Possibility of lease up through recycling and redevelopment. Analysts also expect 7.5% FFO/share growth in 2025.

fast graph

UE also trades below its peers despite its high-quality portfolio. Using an apples-to-apples comparison with EV/EBITDA (because EV includes debt), UE’s 17.3x valuation is lower than its more expensive peers, Federal Realty Investment Trust, Kimco It compares favorably to Realty (KIM), Regency Centers (REG), and Simon Property Group. (SPG), as shown below.

UE vs. Peer EV/EBITDA (find alpha)

Key points for investors

Urban Edge is a promising investment option for those looking to diversify their portfolio with exposure to high-demand retail real estate. With national and regional tenants, UE has demonstrated a solid operating base and occupancy growth by focusing on need-based products and services. Looking to the future, his two major property additions and redevelopments in the past year provide further growth opportunities for UE. Finally, UE remains a Buy at its current price as it has limited debt maturities over the next two years and is undervalued relative to its peers.