Commercial landlords are unable to repay their mortgages…defaults are on the rise…but have local banks reduced their risk?…Bill Gross’ recent banking deals…What the sector looks like through a step-by-step analysis

The dumpster fire that is the commercial real estate sector continues to burn.

Only one of three securitized office loans due in the first nine months of 2023 was paid off, according to Moody’s Analytics.

Here it is wall street journal More from yesterday:

This is the lowest share in the first nine months since at least 2008 and well below the low in 2009, when 47% of loans were paid off.

This rate is well below pre-pandemic rates, when more than 8 in 10 securitized office loans that matured were paid off within a few years.

If you’re a regular Digest reader, you know that we run a year-round “Commercial Real Estate Watch” corner to keep tabs on this vitally important sector of the U.S. economy.

Legendary investor Warren Buffett once said: “You’ll only know who’s swimming naked when the tide goes out.” Well, with Federal Reserve Chairman Jerome Powell saying there is no discussion of cutting interest rates and $1.4 trillion in commercial real estate debt coming due by the end of next year, the tide is turning. It’s going down…

And no sector has more “naked swimmers” than commercial real estate.

***Commercial real estate meltdown in numbers

of WSJ This article explains that many office owners are unable to pay off their old loans because they are unable to get a new mortgage.

To make sure we’re all on the same page, the office sector relies on debt. Landlords take out huge mortgages to purchase buildings at astronomical prices. When the mortgage matures, the landlord can no longer pay off the building in full, so he simply takes out a new mortgage.

The post-COVID-19 remote work trend has led to a rash of office vacancies and a drop in rents (reducing income for owners).

Meanwhile, the Fed’s rate hikes raise financing (and refinancing) costs while also lowering building values (by increasing discount rates).

Given these changes, the math no longer applies to many new commercial mortgages. Return to WSJ for results.

This combination is fueling an increase in debt defaults. The percentage of office CMBS loans that are delinquent has tripled in the past year to 5.75%, Trepp said.

To get a better idea of how bad it is, let’s compare 2023 and 2019.

Before the pandemic, with full office space and low interest rates, landlords were able to roll over maturing debt into new, lower-interest loans. In the first nine months of 2019, 88% of commercial landlords paid off their loans at maturity (by taking out new loans).

Last year, we began to see the first wave of the refinance contagion in a new era of rising vacancy rates, rising interest rates, and declining building values. This means that only 71% of landlords are able to repay their loans.

And this year? This number plummeted to 31.2%.

***Now that we’ve looked at the potential contagion effects of various office REITs, let’s switch focus to a silver lining, and perhaps a deal.

As a result, some homeowners are unable to find new mortgages and pay off their old mortgages.

Now, who is on the other side of the negotiating table in that equation?

Local bank.

As noted in a previous Digest, the commercial real estate sector is closely related to the local banking sector. Most commercial real estate loans are handled by local banks. Bank of America puts the number at about 68%.

Now you may be frowning. It is clear that if commercial real estate is in trouble, local banks will also be in trouble. In fact, in the spring we highlighted his following analysis of JPMorgan.

We expect approximately 21% of our commercial mortgage-backed securities office loan balances to ultimately default, with a loss severity assumption of 41% and cumulative future losses of 8.6%.

Applying the 8.6% loss rate to office exposures would result in banking sector losses of approximately $38 billion…

So what’s different now?

Well, Powell & Co. hasn’t spoken out about a rate cut yet, but Wall Street currently thinks the first rate cut will come in May (and our own Louis Navellier thinks it could happen in January). (claims to be sometime in February).

To be clear, the onset of rate cuts does not mean the end of stress in the commercial real estate sector. But remember, Wall Street is always looking about 12 months ahead. So we want to factor in what the economy and banking sector will look like after another year of easing conditions.

This means bank stocks are likely to rise long before we see any real improvement in bank profits.

*** In this regard, earlier this month, PIMCO co-founder and “bond king” Bill Gross issued a bullish call to regional banks.

From CNBC:

Longtime investor Bill Gross said Thursday that local banks are poised to bounce back from the tailwinds of lower interest rates.

“Regional banks…are benefiting from low interest rates,” Gross said on CNBC’s “Last Call”…

Gross also pointed out that local bank stocks are very cheap right now, and many of them offer high dividends.

“Many of them are at 50% of book value, which is a historically low level. In many cases, yields of 7% plus and payout ratios of 40% provide ample protection.” He said.

Here, Mr. Gross introduces four of his favorite regional bank names and their dividend yields. Bidding over the past few weeks means the yield is slightly lower than the 7% Gross mentions. Still, it’s pretty good:

- Trustworthy person – 6.51%

- Citizen Finance – 6.15%

- Keycorp – 6.69%

- First Horizon – 4.90%

***If we take a step back and assess the regional banking sector from a trading perspective, a bullish trade appears to be starting.

Let’s borrow a tool from one of our trading experts, Luke Lango.

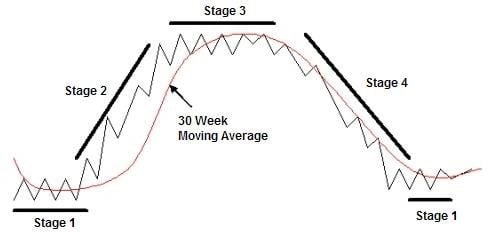

usually digest The reader knows that Luke is his roots. AI trader A trading service based on a market approach called “stage analysis.”

This means that any stock can either go up, down, or stay the same at any given time.

Therefore, every stock is always in one of four unique stages: 1) flat at the bottom, 2) rising, 3) flat at the high, or 4) falling.

Stage analysis is the science of figuring out which of these four stages a stock is in at a particular point in time.

The key to consistently achieving great returns is to find stocks that are about to enter Stage 2 or are already breaking out.

Below is a chart of the SPDR S&P Regional Banking ETF, KRE, with crude oil stage analysis overlaid.

Going back to 2020/2021, we see a Stage 2 bullish explosion (green)… which turned into a Stage 3 top pattern (yellow)… which broke down into a Stage 4 decline (red). …and now appears to be serrated and undergoing stage 1 consolidation (orange).

Source: StockCharts.com

To be clear, Mr. Gross has already pulled the trigger on the trade. He bought the stocks highlighted above.

If you want to follow Mr. Gross into this trade, keep an eye out for it nearing the $49 level. As you can see from the chart above, this is the top of the Stage 1 integration range. KRE could bump its head at this resistance level, resulting in a sharp rebound.

If you are a conservative investor or prefer to follow traditional stage analysis rules, you may want to wait until KRE breaks above this $49 level with heavy volume. This would suggest that the sector is indeed starting a new Stage 2 bullish surge.

Obviously, that means missing out on early profits. But that’s the tradeoff for greater confidence that we’re looking at a true bullish breakout rather than a bearish false out.

We will keep you informed of future developments. But today’s impressive dividend yield is impressive, especially given the historically low book value.

We will notify you of the latest information.

Good evening,

jeff remsberg