This article is part of CNBC Make It millennial money The series details how people around the world earn, spend, and save money.

Just a year after graduating from college, Karun Vij made his dream of owning a property a reality. It started with an “aha” moment.

While pursuing his engineering degree at McMaster University in Hamilton, Ontario, Canada, Vij noticed that rental units near his school charged by the room rather than by the entire house. Things went well. He realized that providing services to students could be more profitable than renting out properties to families and decided he wanted to give it a try.

It took him a few years to save up, but by the time he graduated in 2016, he had enough money to buy a house near McMaster’s campus.

“I knew the area, I liked the area, it wasn’t too expensive, it wasn’t too cheap,” Bisi told CNBC Make It. He added, “It’s a top-five university in all of Canada. It was solid.”

At the age of 26, Viji made a down payment of around 20%. The Hamilton home, valued at $323,904, was rented for $64,781. 7 university students. (CAD to USD conversions were performed using his OANDA conversion rate of 1 CAD to 0.73116 USD on October 3, 2023. All amounts rounded to the nearest dollar.)

Karun Vij at home.

But he had no intention of becoming a full-time landlord. After graduating, Vij worked at a global workplace near Cambridge where he worked as an application engineer and then an account manager at an automation company. The increased rental income and salary allowed Biji to purchase more rental properties in southern Ontario.

Vij, now 33, lives with his wife and daughter in Chicago, where he earns just over $183,000 and owns four Canadian rental properties worth a total of about $2.3 million.

“Buying my first property was one of the most exciting and stressful times of my life,” he says. “I had no idea what it would take to be a landlord, but I knew in my head that this was my job.”

save up to buy your first home

Vij, who grew up in Brampton, Ont., part of the Greater Toronto Area, said she grew up in a “traditional household.” There, he was encouraged to “go to school, get a job as an engineer, doctor, lawyer, etc., and buy one of those jobs,” he said. Two houses. ”

Viji: “I worked.” [his] “I did whatever it took to make money,” he says. That included mowing lawns, delivering groceries, and eventually working door-to-door selling vacuum cleaners.

“No matter the situation, I try to do my best,” he says of his competitive nature. “If I don’t get first place, I’ll go back to square one and try to learn from my mistakes.”

Karun Vij and family.

While at McMaster, Vij was selected by a Fortune 500 company and participated in a two-year paid co-op program. During that time, he earned about $45,000 while living in a rent-free apartment provided by his company, which helped him save for a future down payment.

After graduating with a bachelor’s degree in electrical and biomedical engineering, Vij was hired full-time by the company as an applications engineer.

Investment in rental real estate

Vij’s first rental property was a two-story single-family home with seven rentable rooms two miles from McMaster’s main campus.

As a first-time landlord, Vij was initially surprised by the number of calls he received from tenants for everything from fixing door locks to changing light bulbs.

“I was on the phone at 3 a.m.,” he says. “I had to quickly learn how to put things into perspective and prioritize my key concerns.”

For non-urgent requests, Vij has learned that good communication and follow-through are actually more important to tenants than being available “100% of the day.”

“If you say you’re going to fix something in five days, do it in five days,” he says.

In 2017, Vij put down a deposit of “a few thousand dollars” on a pre-construction condo in Mississauga, a city near Toronto.

Otherwise, the money Viji earned from his job and rental properties went straight to saving for more rental properties. In 2018, he put a 20% down payment on another home in Hamilton worth $316,227. And in 2021, he purchased the adjacent building. The third property was valued at $403,042. He also put his 5% down payment on a pre-construction condo in Milton, Ontario.

In 2022, Vij took a senior position at a company in Chicago. Knowing he had to leave Canada, he hired a property manager and sold the condo he bought in 2017 for about $519,000, more than twice the purchase price.

With that money, he was able to pay off his debts, including student loans, and put a $50,000 down payment on a property in Windsor, Ontario.

Overall, as of October 2023, Vij has 28 rooms available for rent across four properties. Even though his estate is currently worth about $2.3 million, he has no interest in cashing it out.

Karun Vij outside his home in Chicago.

“I don’t care what the price is because I’m never going to sell it. That’s my mindset,” says Vij. “We want to own as many assets as possible that generate cash flow and use the extra cash to buy more assets.”

In 2023, Viji broke even with rental properties. He doesn’t care that he hasn’t made a profit yet. That’s because he expects recently purchased properties to have higher initial costs for furnishing and renovating during the first few years of ownership.

Including utilities, repairs, and property management, his expenses come to about $11,000 a month. He typically brings in that much income from his tenants as well, but the profits he makes in a given month are used to pay down a line of credit or put into a savings account.

“I love debt,” says Vij. “But what I like is only good debt, like a mortgage or line of credit,” he added. “Good debt is debt with a strategy. My long-term strategy. is to buy up as much real estate as possible.”

how he spends his money

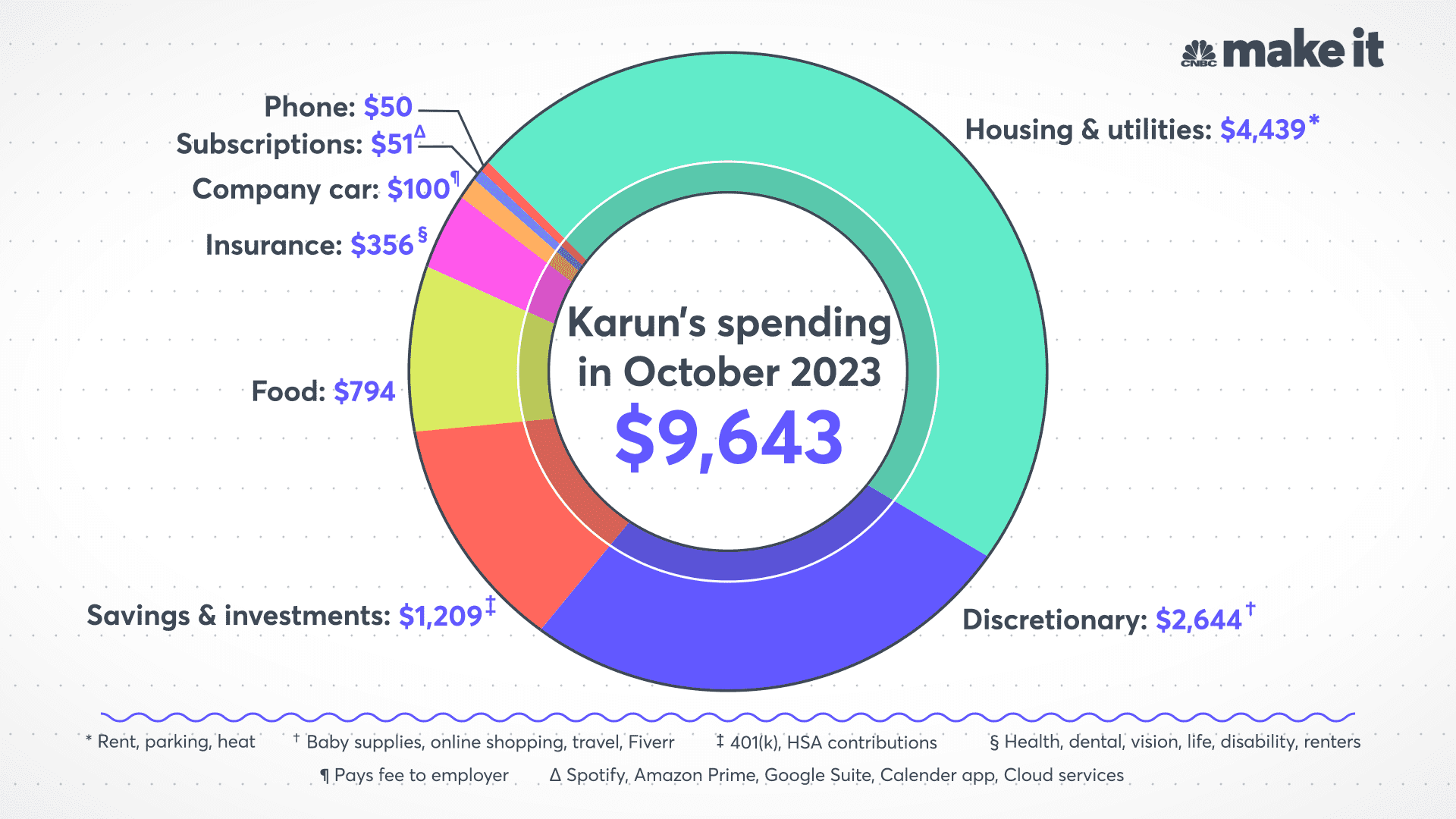

As the sole breadwinner of his family, Viji covers all of his family’s expenses from his own income. Here’s how he spent his money in October 2023.

- Housing and utilities: Rent, parking, and heating for a two-bedroom condo is $4,439.

- Any: Baby Products, Online Shopping, Travel, $2,644 on Fiverr

- Savings and investments: $1,209 (including $1,076 into a 401(k) and $133 into a health savings account)

- food: $794

- insurance: $356 for health, dental, vision, life, disability, and renters insurance

- Company car: $100 fee paid to employer

- Subscriptions and memberships: $51 for Spotify, Amazon Prime, Google Suite, calendar apps, and cloud services.

- phone: $50 for my wife’s cell phone

August, Viji and his wife Seema has welcomed a newborn daughter, so a significant portion of her discretionary spending is on baby items such as bedding and clothing.

In addition to typical benefits like health and dental insurance, Vij receives some great perks through her employer. For $100 a month, you can rent a company car, gas included. Similarly, his cell phone is paid for through work, so he and Seema only spend $50 a month on her cell phone.

Karun Vij and wife Seema at Walt Disney World.

Biji has approximately $18,700 in credit card debt. The amount is unusually high because of a newborn baby and unexpected dental expenses. He also made the strategic choice not to pay it back immediately, saying he would “use that money to buy more assets.”

Vij also has four lines of credit that he uses solely to fund real estate, two of which have outstanding balances totaling $9,798.

As of October 2023, he has over $100,000 in investments, including index funds, corporate stocks, and an inactive company-sponsored pension from when he worked in Canada. Bisi also has just over $73,000 in savings to put toward another property in Windsor, Ont.

Future Plans

Even though the prevailing 25-year fixed mortgage rates in Canada have nearly tripled since 2022, Bisi wants to continue investing in rental properties. In fact, he thinks now is a good time to buy, as home prices in southern Ontario have fallen this year. last year.

He’s also working on plans to convert two neighboring Hamilton homes into larger condominiums, pending some changes to local zoning laws.

“Having a newborn has given me more motivation and ambition in life,” says Vij. “I want to build a life that my family loves and show her daughter that anything in life is possible if you work hard.”

What is the breakdown of the budget? share your story with us For a chance to be featured in a future article.

Don’t miss: Want to be smarter and more successful with money, work, and life? Sign up for our new newsletter.

obtain CNBC’s Free Warren Buffett Investing GuideThis book compiles the millionaire’s #1 advice for everyday investors, the dos and don’ts, and three key investment principles into a clear and simple guidebook.